Insurance Fraud in Times of Crisis

Mar 24, 2020

Simon Staadegaard

The COVID-19 Coronavirus is causing fear, uncertainty and doubt in the form of lockdowns, runs on toilet paper, hospital capacities and many other areas including businesses. Many believe it will lead to an economic recession, the scale of which is still unknown. As with any major catastrophe, fraudsters are looking for new ways to cash in. Insurers must be prepared for the inevitable increase in fraud that occurs during times of crisis. Detecting fraud is not an easy task and requires thorough knowledge about the nature of fraud, how it can be committed and how it’s concealed. People don’t just wake up one day and plan to commit fraud - there are motives behind it. In regular times and in times of crisis, it helps to consider the three elements required to commit fraud.

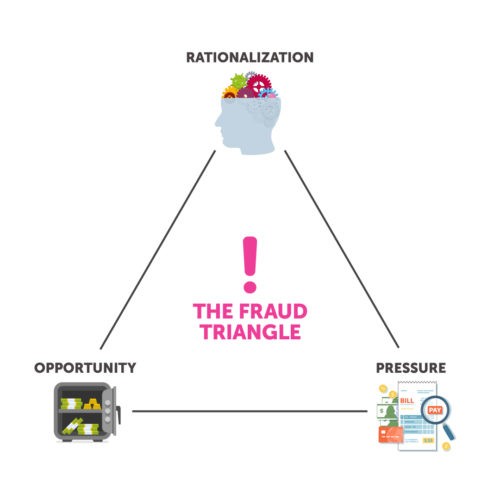

The Fraud Triangle

A criminologist by the name Donald Cressey created the Fraud Triangle in the 1950’s, suggesting there are three elements to committing fraud:

Rationalization: The individual determines that it is okay to commit fraud.

Pressure: This can come from financial distress, a drug or gambling addiction, or the desire to maintain a lavish lifestyle.

Opportunity: This is the unchecked ability to actually commit the fraud.

Financial Pressures

With the present global situation, pressure will mount as businesses find themselves in unplanned financial distress. Many won’t make sales because they are forced to close their doors. Others are already seeing a drastic drop in demand as consumers stop traveling, eating out and gathering in large groups. According to a recent McKinsey & Company brief, business recovery will not start until the end of 2020 or beginning of 2021. As a result, business owners could panic and take drastic steps like burning down their building to cash in on an insurance policy or inflating claims for business disruption. For many, desperate times call for desperate measures. We’ve seen this play out in past economic downturns. Some scams are obvious; others take a keen eye to spot and investigate.

Impact on Carriers

Property and casualty insurance companies will incur underwriting losses directly as a result of the outbreak. Equity market fluctuations and cuts in interest rates to limit the economic fallout will also affect investment income. The most immediate impact will be in the valuation of equity investments and fixed income assets. Claims have already begun to manifest in niche industries like hospitality, tourism, transportation and entertainment as trips, business meetings and events are cancelled, and more people are testing positive. In this regard, rationalization may be easier than ever, even for more “honest” claimants. Twisting the facts slightly to chance a payout seems worth it when there’s no other way to turn, or despite knowing better, the terms of a policy clearly state a particular incident is not covered.

Taking Care of Customers

In times of crisis, insurance carriers bear the burden of making good on their core promise: taking care of their customers when they need it most. When faced with potentially devastating losses, this can be a challenge to properly execute. Carriers can act most swiftly when they are confident they have closed the opportunity for their insureds to commit fraud. Automating assessment of risk and streamlining the detection of fraudulent cases is a proven method of preventing payout on fraudulent claims. While this makes immediate, positive impacts on a carrier’s bottom line, it’s more important side effect is the confident, quick payout of legitimate claims. In the long term, it also shouts a clear message that carriers do not tolerate fraud, stimulating honest behavior.

What’s Next?

Like nearly all businesses, insurance carriers will face a challenging “what’s next” response. While calling together the response teams needed to handle an influx of claims, carriers are also struggling to mobilize employees’ abilities to carry out day-to-day business from their home offices. In addition to the obvious struggles of working from home for those not used to it, there are also hidden challenges: slower or congested home Wi-Fi networks, limited access to company VPN and servers, and a challenge to remain collaborative across teams.

The world will learn many lessons from this current crisis. Some lessons will come immediately while others will be learned over the course of years. Carriers will face interesting decisions on what constitutes “business as usual” moving forward, as both their customers and employees have seen the light of new possibilities, new challenges, and new opportunities to succeed. And it won’t just be businesses who have found new ways to succeed – the fraudsters will as well. They always do. We’ve learned the world was not prepared for this pandemic. Will you be prepared to battle emerging fraud schemes during the next months?